L’avenir de votre enfant commence aujourd’hui

Obtenez 100 $ pour votre REEE lorsque vous commencez à épargner avec nous

Savoir, c’est la moitié de la bataille

Nous sommes là pour vous aider à les aider

Chez Embark, notre seule activité, c’est l’épargne et la planification pour les études. Notre unique objectif est d’aider les étudiants à réaliser leur plein potentiel en simplifiant votre épargne à l’aide d’outils, de conseils et d’un régime d’épargne-études qui convient à votre famille.

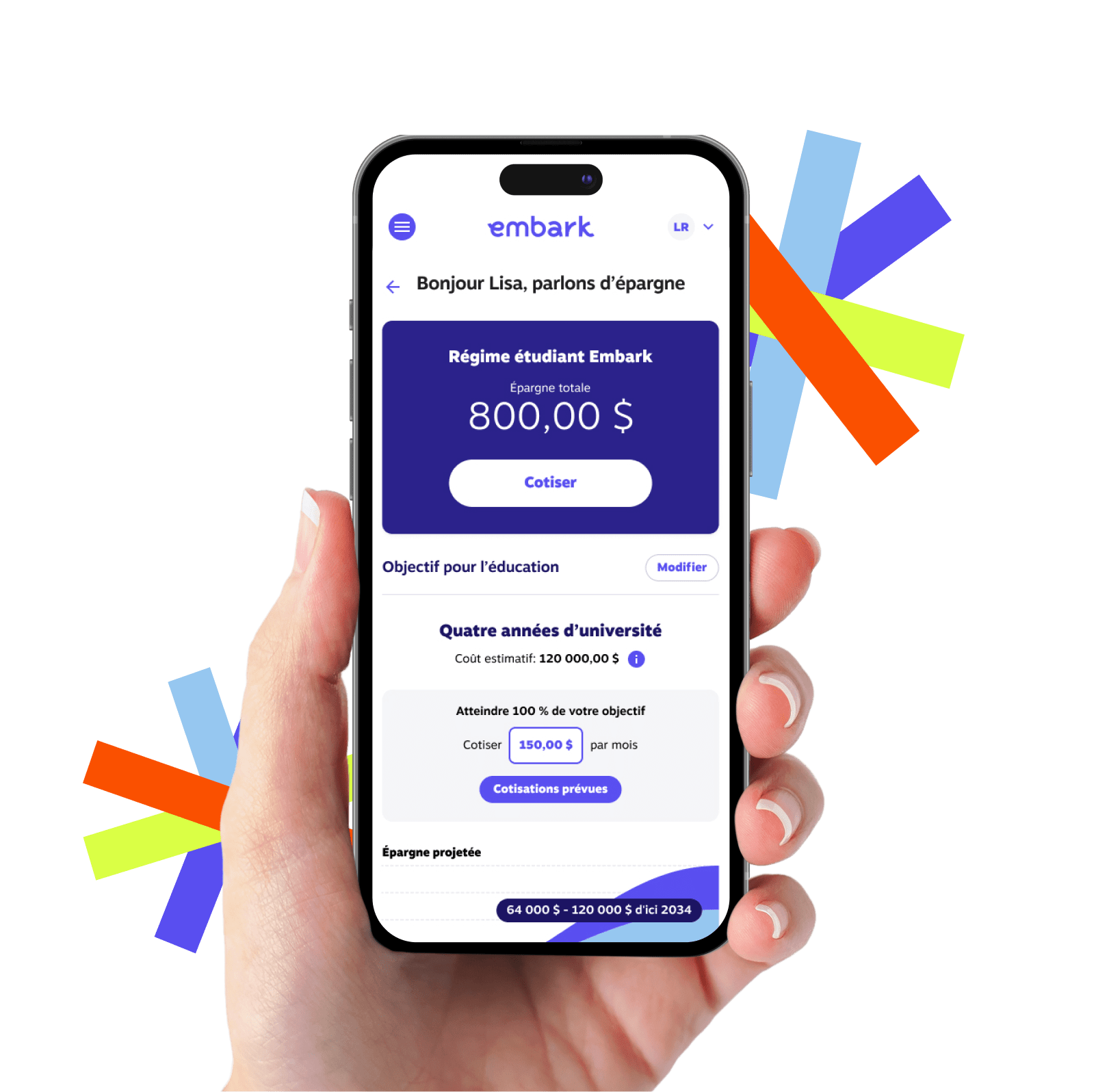

Épargner pour l’avenir n’a jamais été aussi simple

- Un régime d’épargne qui s’ajuste automatiquement au fil du temps

- Des conseils d’expert clairs qui simplifient vos investissements

- Une plateforme numérique innovante qui met l’épargne-études à votre portée

- La capacité de partager votre régime entre plusieurs enfants

Simplifier les REEE

Créons votre avenir

Vous et votre enfant avancez ensemble. Chaque pas vous rapproche de l’avenir que vous lui souhaitez, un avenir où il sera épanoui. Le Régime étudiant Embark est là pour répondre à vos besoins afin d’aider votre enfant à réaliser ses rêves. C’est l’un des gestes les plus importants que vous accomplirez pour préparer l’avenir de votre enfant.

Plus de 60 000

étudiants utilisent le Régime étudiant Embark pour régler leurs frais d’études postsecondaires chaque année.

Plus de 1,2 million

de familles et de bienfaiteurs bénéficient des avantages du Embark.

Plus de 50 ans

d’expérience en épargne-études et en planification pour aider votre enfant à s’épanouir.

Guider vos pas vers la réussite des études

Embark appartient à un organisme sans but lucratif. Cela signifie que tous les profits qui ne sont pas utilisés pour gérer l’entreprise sont reversés à la Fondation Embark étudiant. Nous utilisons ces fonds pour offrir des bourses additionnelles afin d’aider les étudiants à réaliser leur plein potentiel. Nous avons accordé près de 57 millions de dollars aux familles et aux étudiants de tout le pays pour les aider à épargner en vue de leurs études.

Faciles d’accès, et en plus, ils s’occupent de tout pour vous.

Lola O.

Ouvrir la voie du succès

REEE, CELI ou compte d’épargne – Quel est le meilleur ?

Lorsqu’il s’agit de déterminer comment épargner pour les études de votre enfant, vous avez quelques options. Vos amis vous suggèrent peut-être de jeter un coup d’œil à un REEE, à un CELI ou à un compte d’épargne général, mais comment savez-vous lequel est le meilleur ? Jetons un coup d’œil à la façon dont chacun […]

7 minutes

3 façons de mordre dans les taux d’intérêt

Avec la montée en flèche de l’inflation au Canada, les taux d’intérêt sont à la hausse pour aider à maîtriser les prix. Pour les épargnants, c’est une bonne nouvelle. La hausse des taux d’intérêt signifie que plus d’argent est gagné sur ce que vous épargnez. Pour ceux qui sont endettés, cela signifie que plus d’argent […]

4 minutes

À quel moment commencer à épargner pour les études de votre enfant?

Pour nombre d’entre nous, payer les études de nos enfants est un objectif financier à long terme. Cependant, comme l’école est souvent encore loin, l’épargne-études est en général susceptible de passer au second plan par rapport à des besoins plus immédiats. Mais, et c’est un expert qui vous le dit, que vous mettiez peu ou […]

6 minutes